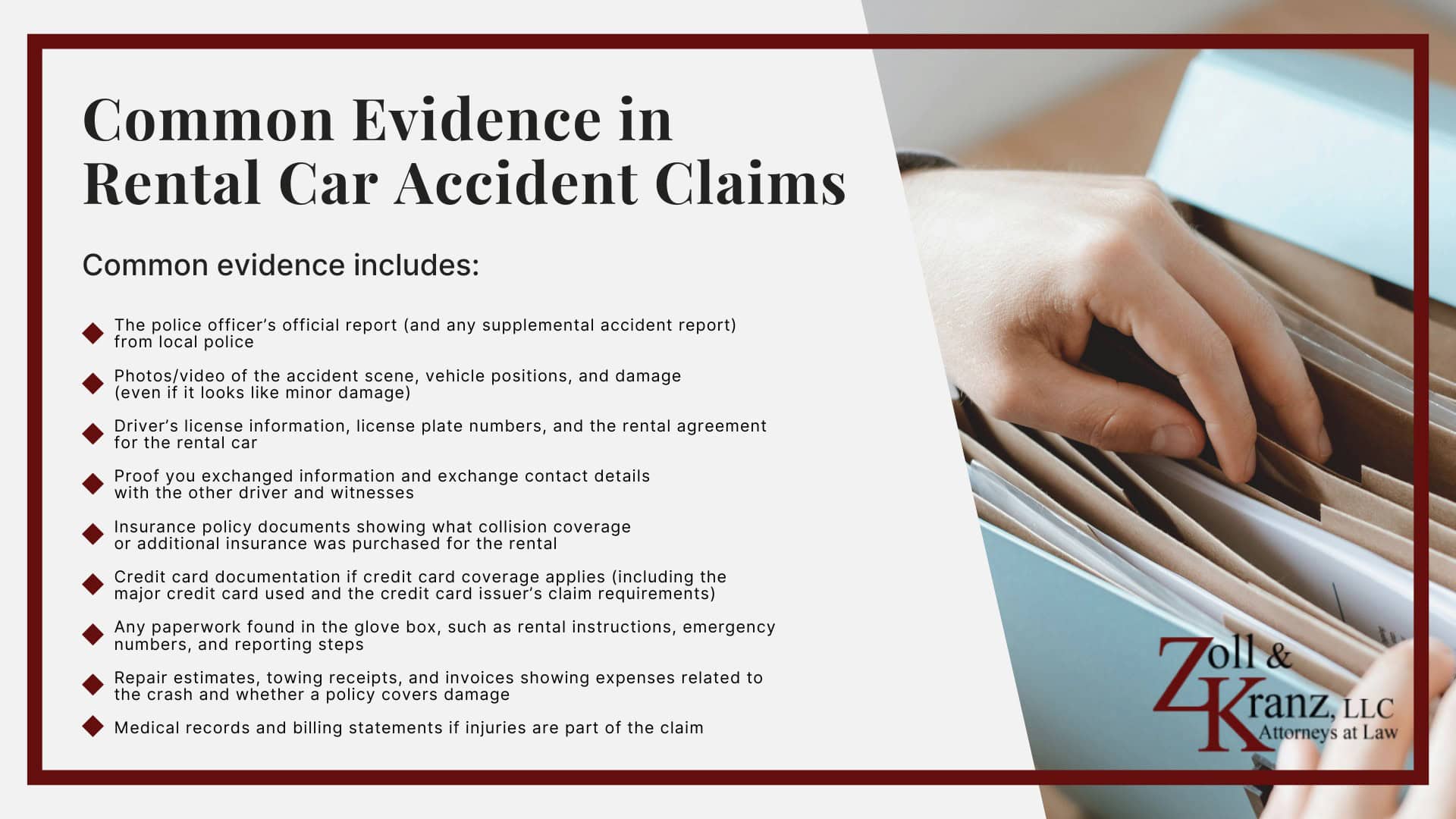

A rental car accident can look like a standard crash at first, but the claim process often becomes more complicated because multiple insurance policies and contract terms may apply to the same incident.

Coverage questions come up fast, and the answers usually depend on specific details like who was driving, who caused the collision, what coverage the renter carried before the trip, and what protection was purchased at the rental counter.

When a crash involves a rental vehicle, you may have to deal with your own insurer, the at fault driver’s liability carrier, and the rental car company at the same time.

If the accident was not your fault, the other driver’s liability insurance should cover damage to the rental vehicle, but you still must report the accident to both the rental car company and your own insurance provider.

Rental companies often have reporting deadlines and documentation requirements, which can create pressure while you are still getting medical treatment and trying to recover.

Insurance coverage can also turn on whether your personal auto policy extends to the rental car. In many situations, personal car insurance does extend coverage to rental cars, including liability insurance for damage to others.

If you do not have personal auto insurance, it is usually wise to purchase temporary insurance to cover a rental vehicle.

If you were involved in a rental car accident without insurance, it is still worth speaking with an experienced auto accident attorney about your options and the facts of the crash.

Driver authorization matters too.

If you allow an unauthorized person to drive your rental car, you may be held responsible for damages they cause, and that issue can complicate both insurance and rental contract disputes.

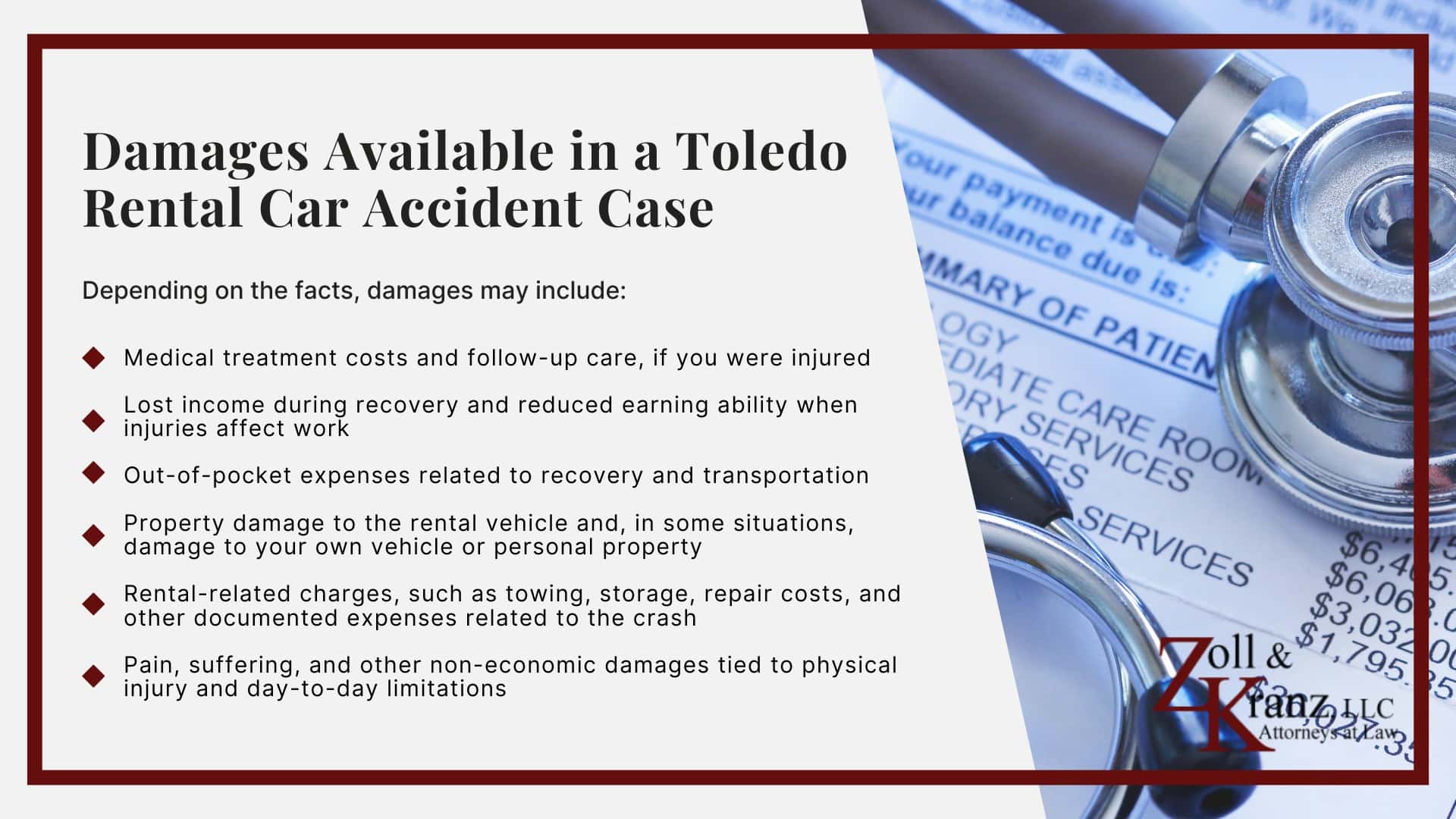

If you sustained injuries in a rental car accident, hiring a personal injury lawyer can help determine whether you are eligible for compensation and identify which coverage applies.

Zoll & Kranz helps clients sort through overlapping policies, reporting requirements, and early insurer tactics that can be used to reduce payment.

Who Is At Fault For A Rental Car Accident?

Rental car accident liability is determined under the same negligence rules as any other crash.

The driver who caused the collision is generally responsible for the damages, and that finding often controls which insurance policies apply first when multiple sources overlap, such as a personal auto policy, a rental agency waiver, or credit card coverage.

Potentially liable parties can include:

- Another driver: If another motorist caused the crash, that driver is typically responsible for injury and property damage through their liability insurance, subject to policy limits and any disputes about fault.

- The renter who was driving the rental car: If the renter caused the collision, a claim may run through the renter’s personal auto policy, since most personal car insurance policies extend liability coverage to rental cars. Depending on what was purchased at the counter, a rental agency waiver or supplemental coverage may also apply, but these products often have limits and exclusions.

- An unauthorized driver of the rental car: If the renter allowed someone not permitted under the rental agreement to drive, that can create a separate liability problem. Violating the rental agreement can void coverage that would otherwise apply and leave the renter personally responsible for costs tied to the crash.

- The rental car company or rental agency: Rental companies are generally not liable for crashes caused by their customers simply because they own the vehicle. The Graves Amendment typically limits that type of vicarious liability. A rental company may still face liability if its own negligence contributed to the crash, such as unsafe vehicle condition, poor maintenance, or defective equipment that played a role in causing the collision.

- A credit card company providing rental coverage: Some credit cards provide rental car protection that can help with certain vehicle damage costs. This coverage usually does not cover liability for personal injury, so it rarely replaces the liability coverage that comes from a driver’s personal auto policy or another driver’s liability insurance.

Because coverage can overlap, fault questions often become insurance priority questions.

A clear liability analysis, backed by crash evidence and the rental paperwork, helps identify which policies apply and where the strongest claim for damages sits.